USD: outlook for August 21-25

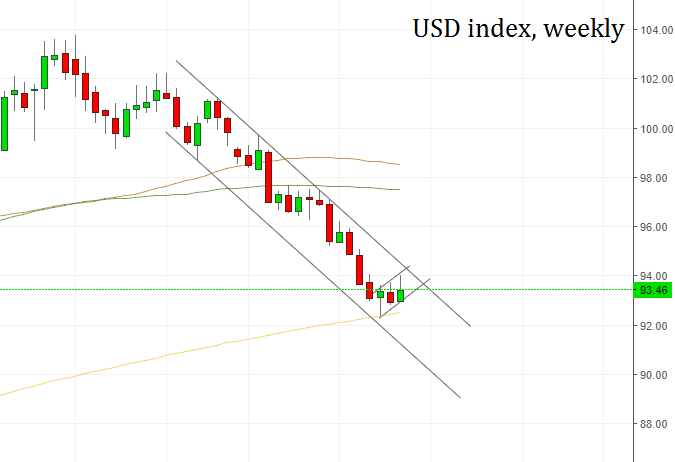

The US dollar index (DXY) got support at 92.80 last week and went up to consolidate between 93.20 and 94.00.

The minutes of the Federal Reserve’s July meeting showed that most central bank officials supported a move towards unwinding the Fed's massive balance sheet in September. The $4.5 trillion balance sheet was built up after the financial crisis to keep borrowing costs low. In addition, markets closely follow the Fed’s discussion about inflation, which has recently shown signs of weakness. Opinions within the Fed slightly differ on this point: some members think that the softness in prices is temporary, while others worry that it will take longer than expected for inflation to rise to 2% target. As a result, the odds are that the Fed will delay a rate hike until inflation picks up. This is not very inspiring for the USD.

In the upcoming days, pay attention to new home sales and crude oil inventories on Wednesday, existing home sales on Thursday and core durable goods orders on Friday. In addition, at the end of the week, world's major central bankers will gather at the Fed’s Jackson Hole Symposium. The Fed Chair Janet Yellen will speak on the topic of financial stability at 17:00 MT time on Friday.

Note that political turmoil in Trump’s administration and the market’s risk aversion will likely reduce the impact of any positive statistics from America and keep the US currency under pressure.

Despite the recent recovery, DXY is still not far from its 13-month lows hit at the beginning of August. It looks like the greenback is correcting up within the general downtrend. A decline below 93.20 will open the way down to 93.00 and 92.50 (200-week MA). Resistance is at 94.00 ahead of 94.90 (50-day MA).